On yesterday’s subscribers’ webinar, economist and DKI Board member, Mish Shedlock, said he thought the US was already in recession. That video will be made public next week, but in the meantime, let’s take a look at the evidence supporting his position:

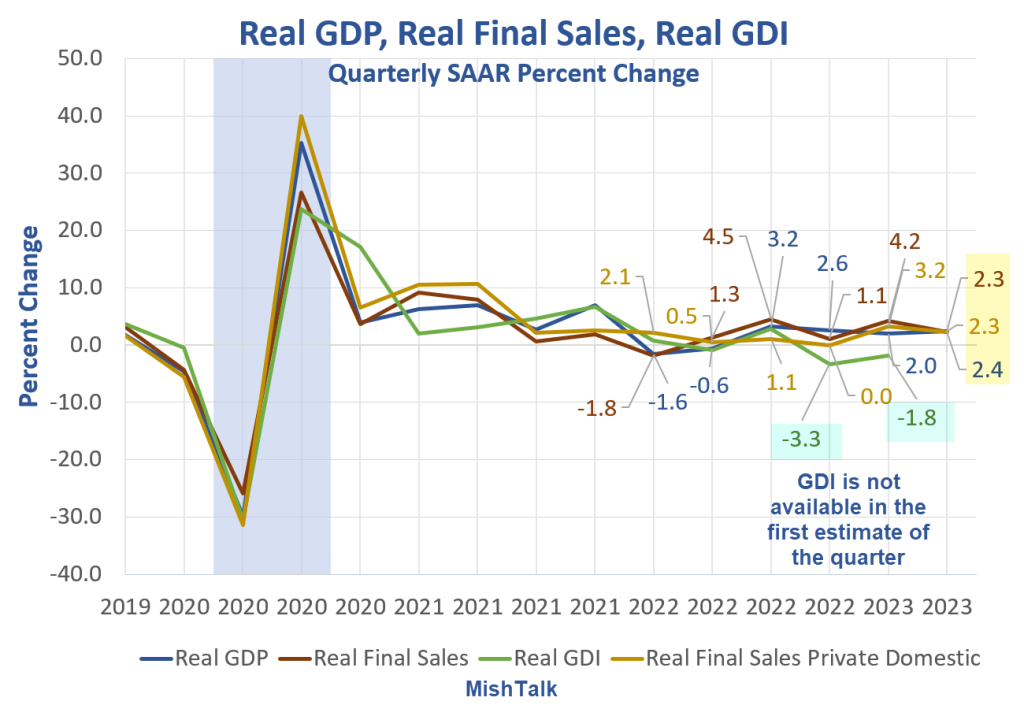

GDP vs GDI:

Mish points out that most economists and market participants focus on Gross Domestic Product (GDP) instead of Gross Domestic Income (GDI). The latter is the sum total of income for the country and over time, the two measures of economic production have to equal each other. However, there has a been a divergence lately, and GDI is negative. It’s possible that GDI is understated right now, but if GDP is overstated instead, then it’s probably already turned negative.

Graph from MishTalk.com

The Bank Narrative Has Shifted:

Earlier this year, when several large banks failed, there were widespread reports that they were tightening lending standards. The feeling at the time was that reducing access to credit would slow the economy. As we’ve gotten to August, the narrative has changed. Now, banks are reporting reduced customer demand for credit. Almost 60% of banks say they have falling demand for loans. The small businesses that wanted financing to expand have stopped asking which would be an early sign of a recession.

The Credit Event Is Here:

Michael Gayed of Tidal Financial has spoken a lot about a coming credit event. His thesis is that many companies took on debt in the years when short-term interest rates were around zero and the 10-year Treasury was below 1%. With short-term rates above 5% and the 10-year above 4% now, many of these companies will have to refinance the cheap debt they took on at much higher rates causing net income to plummet. I agree with his analysis.

DKI Board member, Howard Freedland, pointed out during yesterday’s webinar that over 30% of all debt taken on by commercial mortgage borrowers will need to be financed at much higher rates this year. That’s a huge problem in the real estate business where almost all deals are highly leveraged. To Howard’s credit, when we were preparing for the webinar earlier this week, he mentioned that the stress in the commercial real estate market was going to cause problems for the banks. A day later, Moody’s downgraded 10 banks and is looking at adding more to the list. A round of applause for that unfortunate and correct prediction!

Not So Great Shipping News:

Overall container shipping rates have come down, and FedEx ($FDX) is about to furlough employees. This is right after the country’s third largest less-than-truckload carrier, Yellow Corp. ($YELL), declared bankruptcy. The FedEx announcement on the layoffs came a few months ago, and the container shipping rates are international, but none of this shipping-related data is pointing to strong demand right now.

China and Other Exporting Countries Announcing Huge Declines:

China’s exports fell by 14.5% in July. South Korean exports were down 16.5% in July. According to the Wall Street Journal, “the manufacturing sectors in five out of seven Asian countries, including China and Vietnam, were in contraction last month, pointing to weak underlying demand from the West.” Lower demand for goods is something we’d expect to see in a recession.

Conclusion:

I understand the case for a soft-landing and there is data to support it. However, if Mish is right, and the US has already entered a recession, lower GDI, reduced demand for shipping, reduced demand for goods, and banks reporting plummeting credit demand is exactly what an early-stage recession would look like. DKI is well-hedged for this. If your portfolio leaves you feeling exposed right now, feel free to reach out and we can help.

Information contained in this report is believed by Deep Knowledge Investing (“DKI”) to be accurate and/or derived from sources which it believes to be reliable; however, such information is presented without warranty of any kind, whether express or implied and DKI makes no representation as to the completeness, timeliness or accuracy of the information contained therein or with regard to the results to be obtained from its use. The provision of the information contained in the Services shall not be deemed to obligate DKI to provide updated or similar information in the future except to the extent it may be required to do so.

The information we provide is publicly available; our reports are neither an offer nor a solicitation to buy or sell securities. All expressions of opinion are precisely that and are subject to change. DKI, affiliates of DKI or its principal or others associated with DKI may have, take or sell positions in securities of companies about which we write.

Our opinions are not advice that investment in a company’s securities is suitable for any particular investor. Each investor should consult with and rely on his or its own investigation, due diligence and the recommendations of investment professionals whom the investor has engaged for that purpose.

In no event shall DKI be liable for any costs, liabilities, losses, expenses (including, but not limited to, attorneys’ fees), damages of any kind, including direct, indirect, punitive, incidental, special or consequential damages, or for any trading losses arising from or attributable to the use of this report.